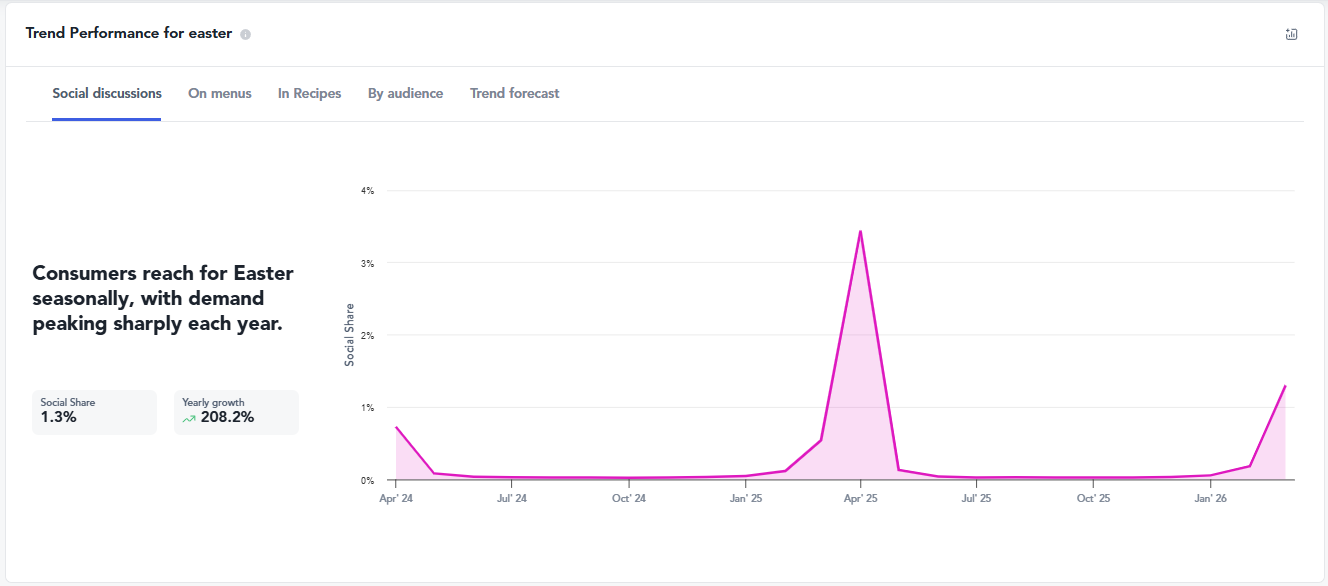

Easter food & candy trends are kind of narrowing. Tastewise data shows cake, cookie, and chocolate egg dominate Easter candy formats in the USA, while earthy ingredients like pistachio (+94% compared to last year) and carrot (+463% in the last 12 months) are gaining fast on Easter confectionery menus. The brands that win 2026 will use familiar formats as the base and contrast-driven flavors as the upgrade.

Already planning your Easter LTO lineup? The Easter 2027 LTO Playbook maps four ready-to-deploy plays across CPG, foodservice, and merchandising.

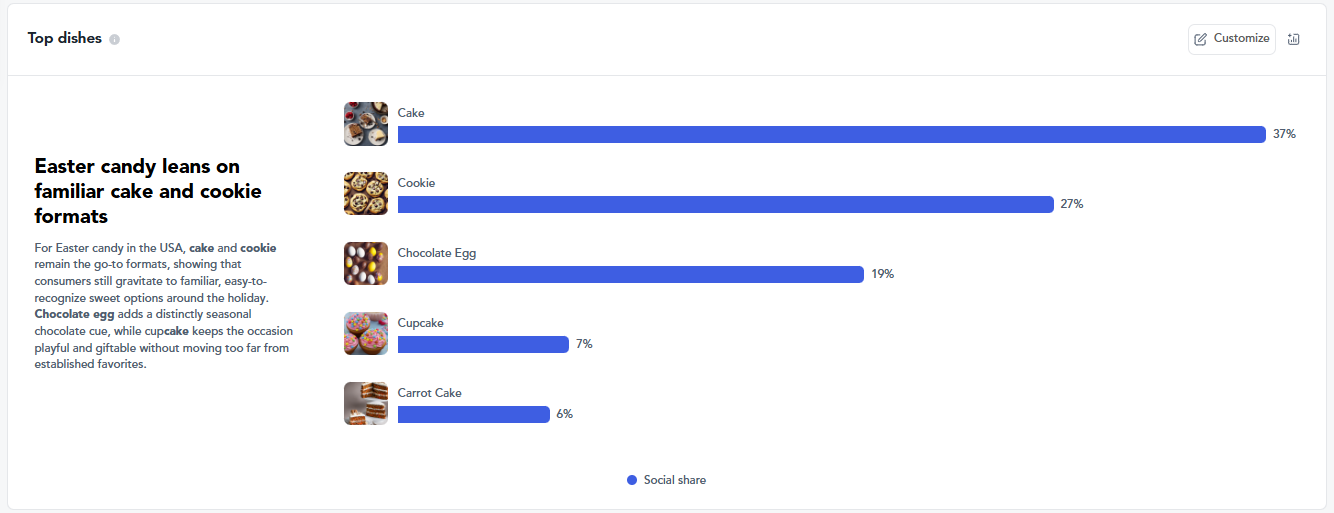

Key takeaways

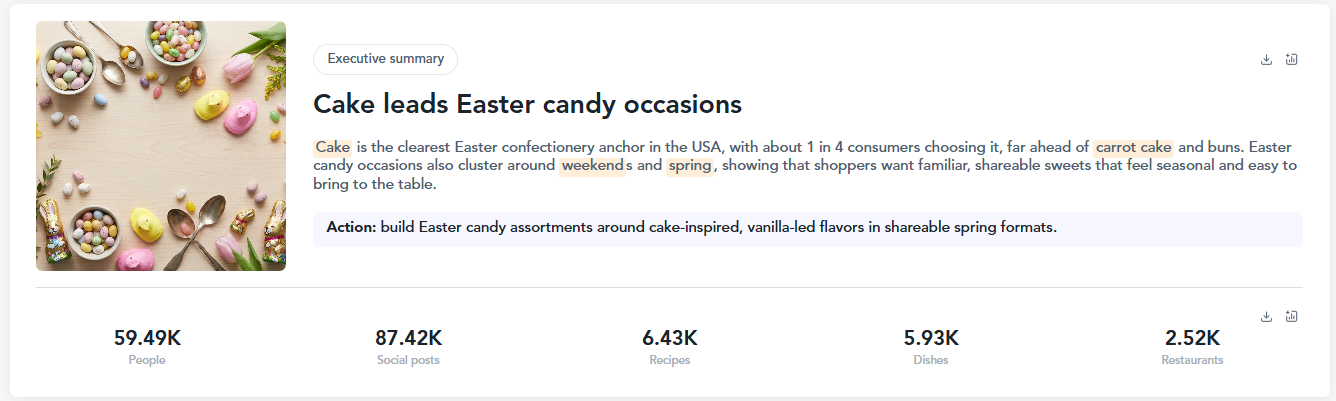

- Cake (37%), cookie (27%), and chocolate egg (19%) are the dominant Easter candy formats in the USA

- Pistachio is up +94% YoY in Easter conversation; carrot is up +463% YoY on Easter confectionery menus

- Weekend indulgence (25%) and spring occasion (15%) are the top consumer motivations driving Easter candy choices

- Consumers are 3x more likely to gather for Easter brunch than Easter lunch, making brunch the primary LTO window

- Earthy flavors (+261% YoY), flavor depth (+161% YoY), and “cozy” (+138% YoY) are the fastest-growing consumer demands in Easter confectionery

The Easter 2026 trade-up problem

The Easter 2026 trade-up problem is a shelf-positioning challenge where familiar, sweetness-led formats no longer justify a premium price point when discount retailers like Aldi and Tesco offer near-identical profiles at low cost. According to Tastewise consumer intelligence data, cake, cookie, and chocolate egg account for the top three Easter candy formats, representing the core of what consumers already expect. That familiarity is the baseline, not the advantage.

The opportunity sits in what consumers are asking for on top of that base. According to Tastewise consumer intelligence data, earthy flavors are up +261% YoY in Easter confectionery conversation, flavor depth is up +161% YoY, and “cozy” is up +138% YoY. These are not niche signals. They reflect a broad consumer appetite for Easter candy that feels considered and seasonal rather than generic and sweet.

The brands most exposed are those whose Easter range reads as interchangeable with everyday confectionery. The brands best positioned are those using familiar formats (cake, chocolate egg) as a recognizable anchor while layering in ingredients that signal craft, season, and provenance.

The R&D formulation playbook: ingredients and cues

The R&D formulation playbook for Easter 2026 is a system for building on proven formats with emerging ingredients that create immediate premium cues, supported by visible inclusions and sourcing claims that close the sale on shelf. Each layer compounds the perceived value without requiring a new manufacturing line.

The earthy ingredient opportunity

According to Tastewise consumer intelligence data, pistachio is up +94% YoY in Easter conversation, driven in part by the Dubai chocolate trend crossing into seasonal gifting. Carrot is up +463% YoY on Easter confectionery menus, making it the fastest-growing earthy cue in the category. Pecan is up +133% YoY, and fruit-acid contrasts including pineapple and blackberry are each up over +50% YoY, pointing to a clear consumer appetite for warmer, earthier, and brighter counterpoints to standard chocolate sweetness. Teams using product innovation intelligence can validate which of these ingredients are still accelerating versus plateauing before committing to a spring run.

The merchandising strategy: visible inclusions

A shopper cannot taste a product on the shelf, so the premium flavor must be readable at a glance. R&D must formulate with visible inclusions such as pistachio pieces on the chocolate shell, carrot-flecked cake bases, or pecan brittle crunch so that Category Managers can sell the visual to buyers before the product leaves the fixture. According to Tastewise consumer intelligence data, berry (20%), strawberry (12%), vanilla (11%), and caramel (10%) round out the top Easter candy ingredients, meaning fruit-forward visual cues (real berry pieces, strawberry glaze) are already legible to consumers as Easter-appropriate.

The sourcing amplifier

Complex earthy flavors perform best when paired with a provenance claim. A pistachio chocolate egg positioned alongside “Single Origin Dark Chocolate” or a carrot cake truffle carrying “No Artificial Dyes” (using natural beetroot colour) creates a multi-signal premium story. The flavor earns attention; the claim provides permission to spend more.

Foodservice operations: cross-utilization for Easter desserts

Foodservice cross-utilization for Easter desserts is a cost-management strategy where kitchens apply existing savory and baking pantry staples to seasonal LTOs, creating high-margin brunch items without single-use pastry sourcing. According to Tastewise consumer intelligence data, consumers are 3x more likely to gather for Easter brunch than Easter lunch, making brunch the highest-ROI window for seasonal LTO investment.

Carrot already sits in most kitchen vegetable prep. A carrot cake brunch board, a carrot and pecan tart, or a spiced carrot glaze on a seasonal donut all draw from existing inventory while landing squarely in the fastest-growing Easter flavor conversation. Pistachios in the nut section become the shell coating on a chocolate Easter egg dessert or the crumble on a cheesecake cup. These are not new sourcing decisions; they are repositioning decisions.

The practical output is a brunch LTO built from what is already on the line, priced at a premium because the flavor story is genuinely seasonal. For a full breakdown of what is performing on menus this season, the Easter menu ideas report covers emerging dish formats and LTO structures by channel.

FAQ: 2026 Easter candy and food trends

According to Tastewise consumer intelligence data, the top Easter food & candy trends for 2026 are built on familiar formats upgraded with earthy, contrast-driven ingredients. Cake (37%), cookie (27%), and chocolate egg (19%) remain the dominant Easter candy dishes in the USA. The fastest-growing flavor signals layered on top of these formats are pistachio (+94% YoY), carrot (+463% YoY), and pecan (+133% YoY), reflecting consumer demand for Easter candy that feels seasonal and sophisticated rather than generically sweet.

The Easter food & candy trends of 2026 are moving toward earthy, layered flavor profiles as the primary differentiators against discount retail. Weekend indulgence (25%) and spring occasion (15%) are the leading consumer motivations, meaning the emotional brief for Easter candy remains reward and seasonality. The change is in how consumers expect that reward to taste: earthy flavors are up +261% YoY and flavor depth is up +161% YoY, signaling that single-note sweetness no longer justifies a premium purchase on its own.

Consumers are seeking premium Easter eggs and desserts because Easter food & candy trends in 2026 reflect a broader appetite for adult complexity in seasonal treats. Single-note sweetness reads as a commodity and commodity products get price-shopped against discount alternatives. As explored in Gen Z eating habits research, younger shoppers expect seasonal food to carry a clear flavor identity, whether earthy pistachio, spiced carrot, or fruit-acid contrast, because these are the flavor languages they use year-round.

We’d love to learn your goals and see how Tastewise fits

We’d love to learn your goals and see how Tastewise fits

Get a personalized demo

Good taste. Wise move.

Your demo request is confirmed. We’ll reach out within one business day to schedule your walkthrough.

What happens next

See what’s driving demand, then turn it into a sell-in story for retailers and operators.

- Connect consumer panels, market trackers, and agents into one evidence view

- Get the “why” behind what’s changing, with explainable demand drivers

- Walk away with a buyer-ready narrative and next steps to activate

Trusted by

“Tastewise is my secret tool for knowing what consumers want next and why.“